Home Loan EMI Calculator with Part Payment: Reduce EMI or Tenure the Smart Way

Posted by yashu sachdeva

Filed in Music 189 views

Buying a home is one of the biggest financial decisions of your life. And once you have taken a home loan, managing it wisely matters just as much as getting it approved. One of the most powerful yet underused tools in a borrower's hands is prepayment. But before you make that move, you need to understand exactly how it affects your loan — and that is where a

home loan prepayment calculator to reduce EMI or tenure becomes your best friend.

Whether you are trying to cut down your monthly burden or close your loan faster, the right calculator gives you the clarity to decide. Let us walk you through everything you need to know.

What Is a Home Loan EMI Calculator?

A home loan EMI calculator is a simple digital tool that tells you how much you will pay every month based on three inputs — your loan amount, interest rate, and repayment tenure. The formula behind it is:

EMI = [P x R x (1+R)^N] / [(1+R)^N – 1]

Where P is the principal, R is the monthly interest rate, and N is the number of months.

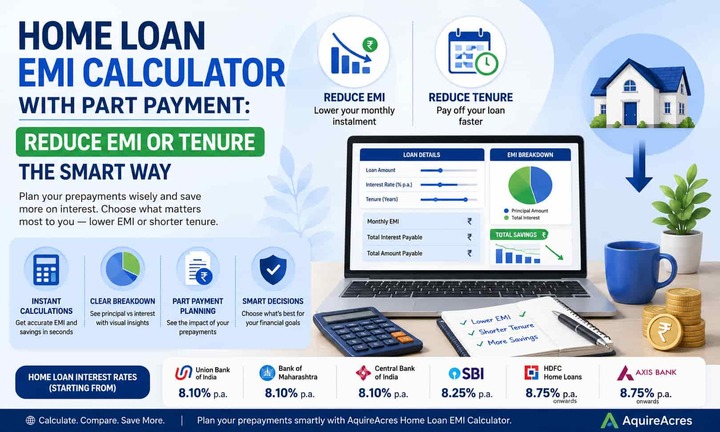

Instead of doing this math by hand, the AquireAcres Home Loan EMI Calculator does it instantly. You adjust the sliders, and you see your monthly EMI, the total interest payable, and a full payment breakdown — right there on the screen.

Why Part Payment Changes Everything

Making a lump sum payment towards your home loan principal is called a part payment or prepayment. When you do this, your outstanding principal drops, which directly reduces the interest calculated going forward. That is the magic of it.

With a home loan EMI calculator with part payment, you can see two things clearly:

Option 1 — Reduce Your EMI: You keep the same tenure but your monthly installment goes down. This improves your monthly cash flow and reduces financial pressure.

Option 2 — Reduce Your Tenure: You keep the same EMI but your loan gets paid off earlier. This saves you a significantly larger amount in total interest.

Most financial advisors suggest reducing tenure over reducing EMI, because the interest savings over years can be substantial. But every situation is different — your income, expenses, and future plans all play a role. The calculator helps you see both outcomes side by side before you decide.

Using a Home Loan EMI Calculator in Excel

Many borrowers also prefer to track their home loan manually using a home loan EMI calculator Excel sheet. This approach is useful when you want full control over your numbers, want to model multiple scenarios, or simply prefer working offline.

In Excel, you can set up your amortization table using the PMT function for EMI, and then manually adjust the principal balance after each prepayment. The spreadsheet then recalculates the remaining interest and tenure automatically.

The benefit of doing this in Excel is customisation — you can add columns for part payments at specific months, change interest rates to simulate floating rate revisions, and track exactly how much interest you have saved. It is particularly helpful for those who want to plan prepayments in advance and visualise their loan closure date on a timeline.

However, for quick decisions and real-time comparisons, an online home loan EMI calculator with part payment like the one on AquireAcres is far faster and easier.

How to Use the AquireAcres Home Loan EMI Calculator

The AquireAcres EMI calculator is built for simplicity. Here is how to use it:

Step 1: Enter your principal loan amount using the slider or input box.

Step 2: Set the loan tenure in months or years.

Step 3: Enter the interest rate applicable to your loan.

Step 4: The calculator instantly shows your monthly EMI, total interest payable, and total amount payable.

You also get a pie chart showing the split between principal and interest — which gives you a visual sense of how much of your money goes towards actual repayment versus interest cost.

For prepayment scenarios, the tool also accounts for floating vs fixed rate conditions. If interest rates are expected to rise, you can model a pessimistic scenario by increasing the rate by 1–3% and see how your EMI changes. If rates are expected to fall, model the optimistic version. This kind of forward planning is especially relevant in today's rate environment.

Home Loan Interest Rates Across Banks

Before jumping into prepayment planning, it helps to know where your loan stands in terms of rate. Currently, home loan interest rates vary across lenders. Some of the most competitive rates include Union Bank of India and Bank of Maharashtra starting at 8.10% p.a., Central Bank of India also at 8.10% p.a., and SBI offering rates from 8.25% p.a. HDFC Home Loans and Axis Bank are at 8.75% p.a. onwards.

Even a 0.25% difference in rate can change your EMI by a few hundred rupees per month — and thousands over the full tenure. Running these numbers through a home loan EMI calculator Excel or online tool helps you compare options clearly.

Should You Reduce EMI or Tenure?

This is the question every borrower asks when they have some extra money in hand. Here is a straightforward way to think about it:

Reducing your tenure saves more money overall. If you have a ₹50 lakh loan at 8.75% for 20 years and you make a ₹5 lakh prepayment in year 3, choosing to reduce tenure could save you lakhs in interest and close your loan several years earlier.

Reducing your EMI improves your monthly liquidity. If your budget is tight or you expect irregular income, a lower monthly obligation gives you breathing room.

The best approach is to model both using a home loan prepayment calculator to reduce EMI or tenure and make a decision based on your actual numbers — not guesswork.

A Few Practical Tips for Smart Prepayment

You do not need a windfall to make a difference. Even small, consistent prepayments add up. Here is what works in practice:

Annual bonus? Put a portion toward prepayment in the first 5–7 years of the loan, when the interest component in your EMI is highest.

Received a tax refund? Even ₹50,000 to ₹1 lakh towards principal in the early years can save you more than double that in interest by the end.

Getting a salary hike? Consider increasing your EMI slightly rather than spending the increment. This effectively reduces your tenure without a lump sum requirement.

Always check with your bank whether there is a prepayment penalty — most floating rate home loans in India do not charge one, but it is worth confirming.

Final Thoughts

Managing a home loan smartly is not just about picking the right bank or rate — it is about staying in control throughout the repayment journey. Tools like the AquireAcres home loan EMI calculator with part payment make that control accessible to everyone.

Whether you prefer to run scenarios through a home loan EMI calculator Excel sheet or use an instant online tool, the core idea is the same — understand your numbers, plan your prepayments, and decide whether you want to reduce EMI or tenure based on your financial reality.

Your loan is a long-term commitment. Using the right tools to manage it can save you years of repayment and lakhs of rupees. Start calculating today at

Frequently Asked Questions (FAQs)

Q1. What is the difference between reducing EMI and reducing tenure after a home loan prepayment?

When you make a part payment, your bank gives you two choices. Reducing EMI means your monthly installment goes down while the loan duration stays the same. Reducing tenure means your EMI stays the same but your loan closes earlier. Reducing tenure is usually more beneficial financially because it saves more total interest over the life of the loan.

Q2. Can I use a home loan EMI calculator Excel for part payment planning?

Yes, absolutely. Excel allows you to create a full amortisation schedule using the PMT function and manually adjust the principal balance after each prepayment. You can model multiple scenarios — for example, making one large prepayment versus several smaller ones — and compare total interest savings across each option. It is a great tool for detailed, offline planning.

Q3. How does a home loan prepayment calculator help reduce EMI or tenure?

A home loan prepayment calculator to reduce EMI or tenure shows you the exact impact of a lump sum payment on your loan. You enter your current outstanding principal, interest rate, remaining tenure, and prepayment amount. The calculator then shows you the revised EMI (if you choose to reduce installment) or the new tenure (if you choose to close the loan faster), along with total interest saved.

Q4. Is it better to make one large prepayment or multiple smaller ones?

Both strategies work, but timing matters more than size. Prepayments made in the early years of the loan save more interest because a higher proportion of your EMI goes towards interest during that period. Multiple smaller prepayments spread over the first 5–8 years can often be more effective than one large payment made later in the tenure.

Q5. Are there any charges for home loan prepayment in India?

For floating rate home loans, the Reserve Bank of India (RBI) has directed banks and NBFCs not to charge any prepayment penalty from individual borrowers. However, fixed rate home loans may still carry a prepayment charge, typically ranging from 1% to 3% of the prepaid amount. Always check your loan agreement or contact your lender directly before making a large prepayment.